Where the Yuan Is Winning: De-Dollarization by Corridor, 2020-2026

The yuan is only 3% of global payments - but that average hides a bimodal reality. In specific bilateral corridors, it has already won.

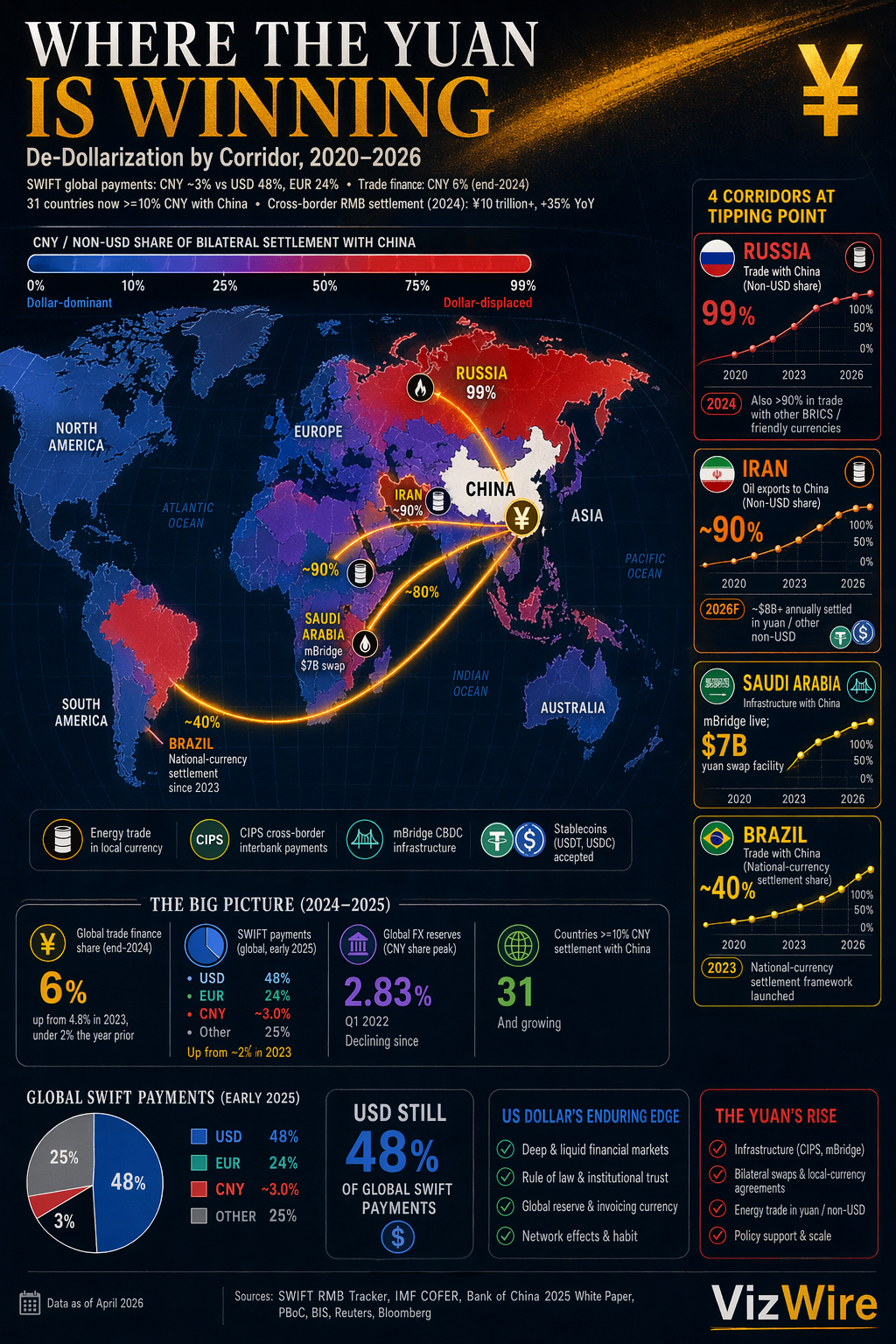

The headline statistic on yuan internationalization looks like a dud: the renminbi accounts for just roughly 3% of global payments tracked by SWIFT, versus 48% for the US dollar and 24% for the euro. Read only that number and de-dollarization looks like a rounding error.

The number is misleading because it is an average. In specific bilateral corridors - the ones that matter most geopolitically - the yuan has already won. In others it has barely moved. The real story of 2020 to 2026 is the bimodal distribution hiding underneath the global average.

The global view: small but steady

Aggregate yuan usage has grown, but slowly and unevenly across categories:

| Metric | Recent reading | Trend |

|---|---|---|

| Yuan share of SWIFT global payments | ~3.0-3.5% (2025) | Up from ~2.0% in 2023 |

| Yuan share of global trade finance | 6% (end-2024) | Up from 4.8% (2023), under 2% the year prior |

| Yuan share of global FX reserves | Below 2.83% | Declining from Q1 2022 peak |

| USD share of SWIFT payments | ~48% | Roughly flat |

| EUR share of SWIFT payments | ~24% | Roughly flat |

Trade finance is where aggregate growth is fastest - roughly tripling in two years. SWIFT payments have drifted up modestly. FX reserves have actually declined from their 2022 peak, meaning central banks are not buying the yuan story as aggressively as commercial traders are.

The corridor view: total takeovers

Zoom to specific country-pairs and the picture inverts:

| Bilateral corridor | Yuan / non-USD share | Year |

|---|---|---|

| Russia ↔ China trade | ~99% in national currencies (ruble/yuan) | 2024 |

| Russia ↔ other BRICS | ~90% in "friendly" currencies | 2024 |

| Iran oil exports to China | ~90% non-USD (~$8B+ annually) | 2026 |

| Saudi Arabia ↔ China | mBridge rail live; $7B yuan swap facility | since 2024 |

| Brazil ↔ China | national-currency settlement agreement in force | since 2023 |

31 countries now use the renminbi for at least 10% of their payments with China, per SWIFT. Cross-border RMB settlement exceeded ¥10 trillion in 2024 - a 35% year-on-year increase.

Where the tipping happened

Three forcing functions pushed specific corridors past 50% non-USD:

- Sanctions exposure. Russia (2022) and Iran (ongoing) effectively lost access to dollar rails. Their trade did not stop - it redirected.

- Energy sellers diversifying payment. Saudi Arabia's June 2024 decision not to renew exclusive dollar-pricing removed a major political constraint. Iran's April 2026 Strait of Hormuz tolls are paid in CNY and stablecoins, not USD.

- Infrastructure maturity. CIPS - China's yuan clearing network - and mBridge, the cross-border CBDC pilot with UAE, Thailand, and Hong Kong, now provide plumbing that did not exist in 2020.

Where the dollar is still untouchable

The yuan has not dented:

- FX reserves. USD still holds roughly 58% of allocated reserves; yuan holdings have fallen from their 2022 peak.

- Invoicing outside the China bloc. Europe, Latin America ex-Brazil, and most of Africa still bill in USD or EUR.

- Safe-haven demand. When markets panic, capital still flees to dollars, not away from them.

The 2026 picture

The yuan is not the next reserve currency. It is, however, the default settlement currency for a specific coalition - Russia, Iran, Venezuela, and increasingly any country that is sanctioned or wary of becoming so. Saudi Arabia and Brazil are optional adopters in that bloc. Europe and Japan are not.

The question for the next five years is not whether the yuan "replaces" the dollar. It is how many more corridors tip from majority-USD to majority-CNY - and whether countries that are not sanctioned (Indonesia, Egypt, Turkey, Argentina) start choosing yuan rails voluntarily, for the optionality alone.

Sources

- SWIFT — Global Currency / RMB Tracker document centre

- SWIFT — RMB Tracker (July 2025)

- Trade Treasury Payments — RMB share of global payments, SWIFT data

- Deutsche Bank — Charting the Renminbi's rise as a global currency (June 2025)

- Federal Reserve — Internationalization of the Chinese renminbi: progress and outlook

- Asia House — The Renminbi's Rise and its Accelerated Use in Global Trade Finance

- BBVA Research — Riding the Waves: Stocktaking RMB Internationalization (Feb 2025)

- Politics Today — Russia and China settle 99% of trade in national currencies

- CSIS — CRINK Economic Ties: Uneven Patterns of Collaboration

- Wikipedia — Dedollarisation