Tesla Is Betting $25 Billion That Cars Are the Past

Tesla tripled its capex to $25B, ending Model S/X production to build robots and robotaxis. The car company is becoming something else entirely.

Tesla made $21 million selling cars last quarter. Twenty-one million. That is roughly what a single McDonald's franchise cluster generates in a year. And on the same earnings call where that number landed, the company announced it would spend $25 billion this year — not on cars, but on robots, robotaxis, AI chips, and a future that may or may not arrive on schedule.

This is not a pivot. It is a controlled demolition of the old Tesla, with the new one being built on top of the rubble.

The $25 Billion Bet

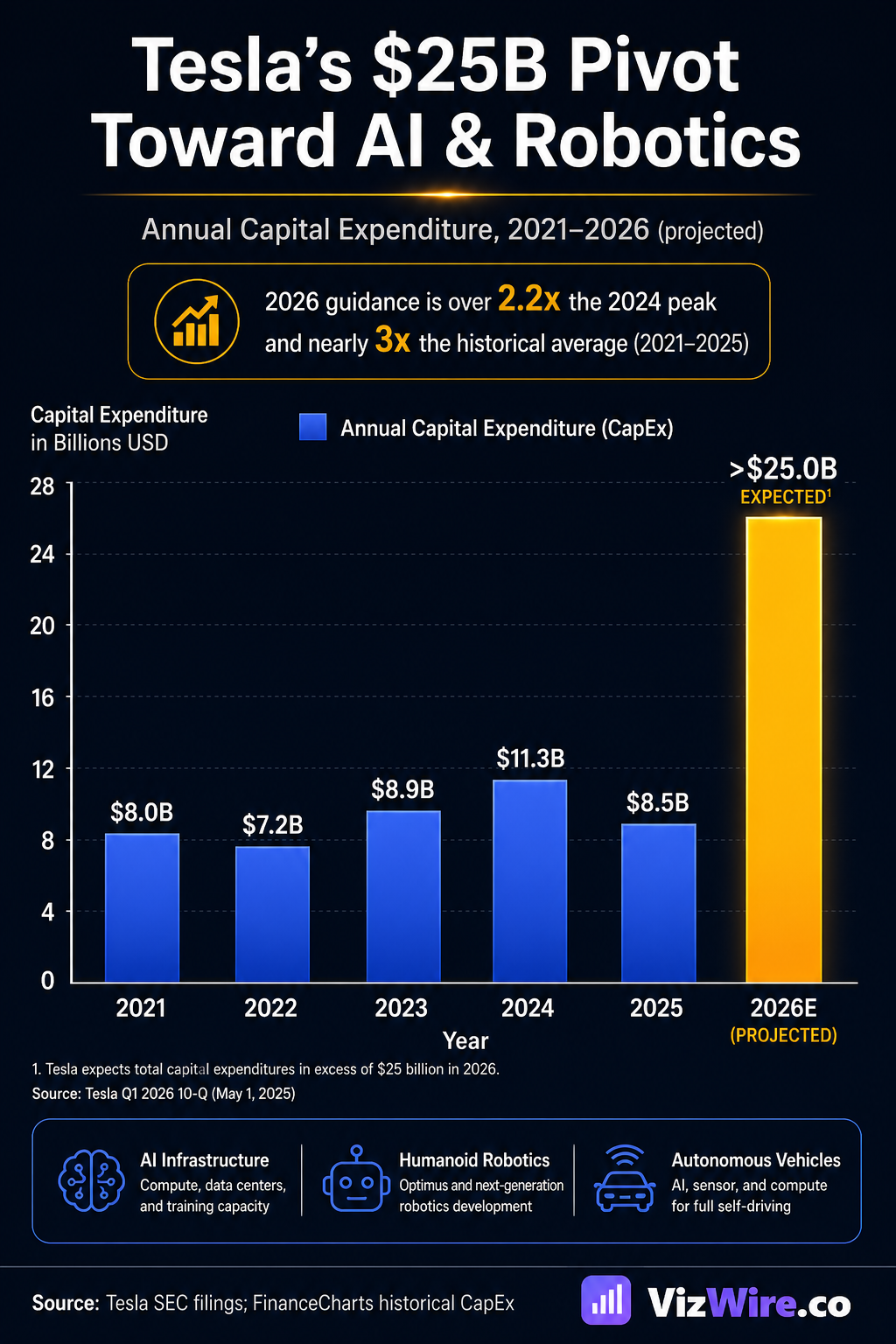

To understand how dramatic this spending plan is, you have to see it in context. Tesla spent $6.5 billion on capital expenditures in 2021. By 2024, that had climbed to $11.3 billion — the previous peak. Then in 2025, it actually pulled back to $8.5 billion. Now? The 2026 target is $25 billion, raised from an already-aggressive $20 billion guidance earlier this year.

View raw data

| Year | CapEx (Billions USD) |

|---|---|

| 2021 | $6.5B |

| 2022 | $7.2B |

| 2023 | $8.9B |

| 2024 | $11.3B (previous peak) |

| 2025 | $8.5B |

| 2026 (target) | $25.0B |

That gold bar is not a typo. Tesla plans to spend more in 2026 than it did in 2021, 2022, and 2023 combined. And CFO Vaibhav Taneja confirmed the obvious consequence: Tesla will be free-cash-flow negative for the rest of the year. Q1 capex was $2.49 billion, which means Tesla needs to spend roughly $7.5 billion per quarter for the rest of the year to hit the target.

Where is all that money going? Four places: Optimus humanoid robots, the Cybercab robotaxi, AI compute infrastructure, and a chip fabrication facility that Tesla and SpaceX are building together — reportedly the largest chip fab ever.

The Car Business Is Running on Fumes

Here is the part that does not add up — or rather, adds up to an uncomfortable number. Tesla's GAAP profit in Q1 2026 was $491 million. Respectable on the surface. But strip out the non-core revenue and the picture changes entirely.

View raw data

| Category | Amount | % of Total |

|---|---|---|

| Regulatory Credits | $297M | 60.5% |

| Bitcoin Sales | $173M | 35.2% |

| Core Auto/Battery Profit | $21M | 4.3% |

Just 4.3% of Tesla's reported profit came from actually building and selling vehicles. The rest? $297 million in regulatory credits sold to other automakers, and $173 million from selling Bitcoin. That regulatory credit revenue is shrinking, too — it dropped 44% year-over-year in Q3 2025 as competitors catch up on EV compliance.

The top-line numbers look better: $22.38 billion in revenue, up 16% year-over-year. Gross margin hit 21.1%, up 478 basis points. But Electrek noted those gains were partly from one-time benefits related to warranty and tariffs. And there is the inventory question: Tesla produced 408,386 vehicles but delivered only 358,023 — a gap of over 50,000 cars sitting in lots.

View raw data

| Metric | Units |

|---|---|

| Vehicles Produced | 408,386 |

| Vehicles Delivered | 358,023 |

| Inventory Gap | 50,363 |

Death of the Model S — Birth of Optimus

The most visceral sign of the transformation is happening at Fremont. Tesla is ending production of the Model S and Model X in early May, closing the book on vehicles that defined the brand for over a decade. The line will not sit idle. Within four months, that same factory floor will begin producing Optimus humanoid robots, with production starting in late July or August 2026.

Musk described the conversion speed as "insanely fast". But he was more candid about what comes next. Optimus has over 10,000 unique parts, and Musk warned that initial output will be "quite slow", adding that it is "literally impossible to predict" the production rate.

"It will move as fast as the least lucky, slowest, dumbest part in the entire 10,000," Musk said during the earnings call.

The ambition behind those cautious words is staggering. The Fremont line is designed for 1 million robots per year. A second-generation line at Giga Texas is being prepared for 10 million per year starting in 2027. The long-term price target? Under $20,000 per unit. For context, in January 2025, Musk predicted 10,000 Optimus units that year. By January 2026, he acknowledged zero robots were performing useful work at Tesla facilities.

View raw data

| Date | Event | Detail |

|---|---|---|

| May 2026 | Model S/X production ends | Fremont factory |

| Mid 2026 | Optimus V3 reveal | Third-generation design |

| Jul-Aug 2026 | Optimus production begins | Fremont line |

| Late 2026 | Cybercab ramp begins | Exponential scaling target |

| 2027 | Giga Texas Optimus line | 10M/year capacity |

The Robotaxi Reality Check

If Optimus is Tesla's moonshot, the robotaxi is supposed to be the bridge — the product that proves autonomous driving works and starts generating revenue before the robots arrive. But the bridge is shaky.

Tesla's robotaxi service launched in Austin on June 22, 2025, with safety monitors in modified Model Y vehicles. Eight months later, the status check was sobering: roughly 42 vehicles operating, 19% availability, and a crash rate 9 times worse than human drivers.

View raw data

| Metric | Tesla | Waymo |

|---|---|---|

| Active Vehicles | 42 | 2,500 |

| Availability | 19% | ~95% |

| Crash Rate (per 100K mi) | 1.8 | ~0.1 |

| Cities Operating | 1 | 5 |

To put the crash rate in perspective: Tesla logged roughly 9 crashes in about 500,000 miles — one crash per 55,000 miles. The human average is one police-reported crash per 500,000 miles. Waymo, meanwhile, operates 2,500 active robotaxis across five US cities — including roughly 200 in Austin alone, compared to Tesla's 42.

Tesla says it is expanding to seven more cities in the first half of 2026 and targeting roughly a dozen US states by year-end. Cybercab production has officially begun, with output expected to ramp exponentially toward the end of the year. But Musk himself admitted Tesla needs 10 billion miles of data for safe unsupervised self-driving — a threshold the fleet will not hit until July 2026 at the earliest.

The Market's Verdict

Wall Street is not sure what to make of all this. Tesla shares fell 3.7% the day after earnings, and the stock is down 17% year-to-date in 2026. TD Cowen cut its price target to $490, citing the elevated capex and FSD strategy concerns.

The valuation math is surreal. Based on core automotive profits, Tesla trades at a P/E of roughly 657. Its $1.4 trillion market cap is not a bet on cars. It is a bet on a future where Tesla is a robotics company, an autonomous driving network, and an AI infrastructure player — all at once.

Whether that future arrives is genuinely unknowable. What we do know: Tesla is burning every bridge to the old business to get there. The Model S is dead. Free cash flow is gone for the year. And $25 billion is being poured into products that do not yet exist at scale. The car company is becoming something else entirely — and it is happening right now.

Sources

- TechCrunch — Tesla just increased its spending plan to $25B

- Electrek — Tesla Q1 2026 financial results

- Electrek — Tesla Optimus production at Fremont

- Electrek — Tesla Robotaxi status check: 8 months in

- QuantoSei News — Tesla Q1 2026 earnings analysis

- FinanceCharts — Tesla Annual Capital Expenditures

- Good Car Bad Car — Tesla Q1 2026 / TD Cowen analysis